Romania & Bucharest Retail Guide 2026

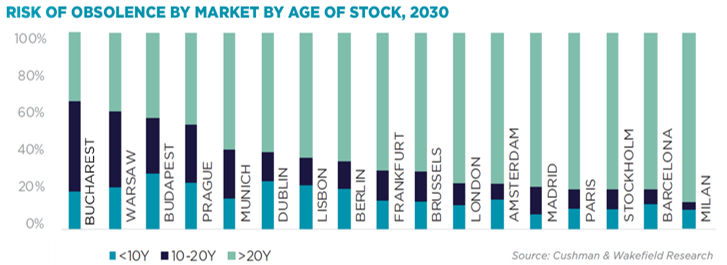

Bucharest, December 2024 – With an average age of approximately 11 years, the Bucharest office stock ranks among the youngest across Europe and the CEE region. This provides a significant advantage for landlords in attracting and retaining tenants, as the city’s office spaces are less likely to face obsolescence in terms of technology, construction quality and sustainability standards over the next 5 – 6 years, according to data from the Cushman & Wakefield Echinox real estate consultancy company.

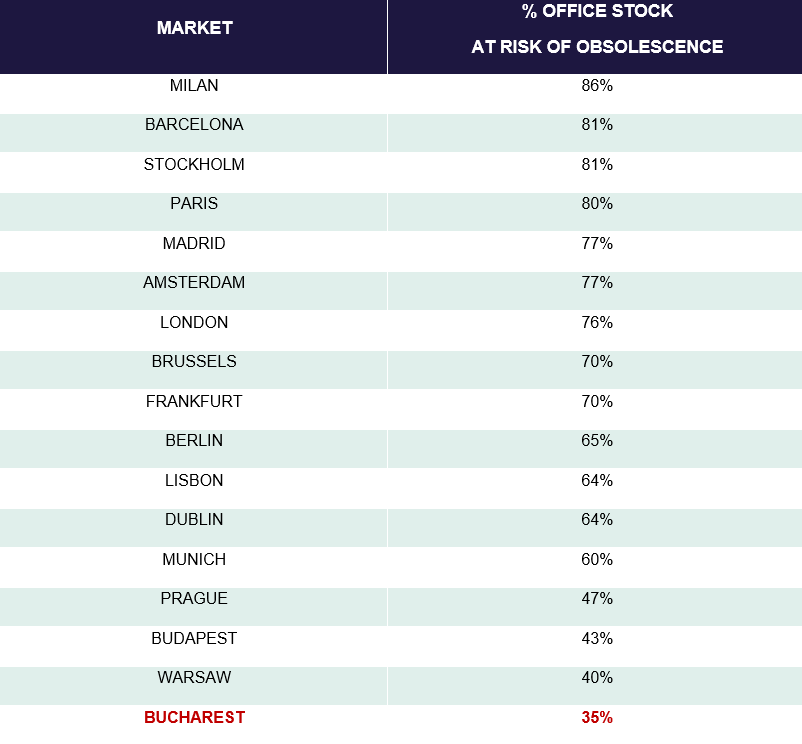

In total, over 170 million sq. m of office spaces are at risk of becoming obsolete in 2030 across 16 European markets, according to the Rethinking European Offices report, produced by Cushman & Wakefield.

This is equivalent to more than 6 times the total office stock in Central London. In volume terms, the majority of this ‘at risk’ stock is in Western European markets.

Close to 80% of stock is at risk of obsolescence in that particular region in markets such as Amsterdam, Barcelona, London, Madrid, Milan, Paris and Stockholm.

In contrast, the CEE markets – Bucharest, Budapest, Prague and Warsaw – have lower risks of obsolescence (averaging just 43%), thus reflecting that much of the built stock has been delivered over the last couple of decades. Since 2004, the office stock in Eastern European markets has more than doubled, while in Western Europe most markets have seen the stock grow by less than 20%.

Compared with the regional average, Bucharest’s office stock is even younger, with nearly half of the existing 3.41 million sq. m of office spaces being built during the last decade. This reduces the city’s equivalent obsolescence risk to just 35%, the lowest among the analyzed markets.

Madalina Cojocaru, Partner Office Agency at Cushman & Wakefield Echinox: “Occupiers are today focused on securing the best-in-class, grade A office spaces in central or semi-central areas, with access to a wide range of amenities and which meet the latest environmental and sustainability standards. This is important in terms of attracting employees and creating the best working environment. Across Europe, grade A leasing accounts for around 50% of the total take-up, up from 40% before the pandemic and from around 33% over a decade ago. In Bucharest, 83% of the YTD transaction volume occurred in grade A buildings, which account for 79% of the total stock in the city.”

Madalina Cojocaru, Partner Office Agency at Cushman & Wakefield Echinox: “Occupiers are today focused on securing the best-in-class, grade A office spaces in central or semi-central areas, with access to a wide range of amenities and which meet the latest environmental and sustainability standards. This is important in terms of attracting employees and creating the best working environment. Across Europe, grade A leasing accounts for around 50% of the total take-up, up from 40% before the pandemic and from around 33% over a decade ago. In Bucharest, 83% of the YTD transaction volume occurred in grade A buildings, which account for 79% of the total stock in the city.”

The Bucharest office market has shown clear signs of stability during the first 9 months of the year, with the leasing activity reaching a total of 261,700 sq. m. While this represents a 25% decrease compared with the same period last year, the volume remains at a satisfactory level, reflecting resilience in tenant demand despite the existing market challenges.

This decrease was expected in a context where not a single building was delivered throughout 2024 and also when considering that 2023 was a record year for the Bucharest office market in terms of total take-up.

Across Western markets, the risk is not uniform. Munich (60%), Lisbon (64%), Dublin (64%) and Berlin (65%) are better positioned compared with other markets tracked, as an important part of the stock has been developed over the past two decades. In London, the analysis suggests that 76% of the existing offices may become obsolete by the turn of the decade. With regulations already in place, it should accelerate the pace of change, especially in an improving economic landscape.

Moreover, many landlords are actively upgrading or redeveloping buildings in order to meet these needs and the growing demands from occupiers. On the other hand, although higher rents are at odds with corporate cost control, the central locations of those buildings and the amenities they provide are critical factors for success which should translate in high levels of both talent attraction and retention.

In this context, we anticipate a growing divide between best-in-class, centrally located assets and those in peripheral locations, where the vacancy risk is often greater. Landlords need to understand their spaces and whether repositioning or repurposing is the best strategic approach.