European Investment Atlas Q1 2026

Bucharest, March 2022: The local real estate market has rapidly adapted to the new social and business environment, largely countering the imbalances stemming from the restrictions imposed during the state of alert. Moreover, we can notice an upward trend in all market segments, even though there are still a few challenges, such as the increasing prices for construction materials, utility costs, inflation, decreasing purchasing power and also finding the best levers to get employees back to their offices.

Cushman & Wakefield Echinox performed an in-depth analysis of the main real estate market indicators and of the opportunities that come with the changes in consumption habits, working patterns, etc., while also highlighting the main challenges faced by this sector.

Real estate investment market: More transactions and a larger volume compared with 2018-2019

The investment market is an important indicator in terms of the attractiveness of the real estate segment. Thus, the market liquidity pertaining to transactions with income-producing properties remained high in 2020 and 2021, corresponding to a total volume of EUR 1.83 billion, compared with EUR 1.67 billion in 2018-2019. In total, 78 assets have been traded over the past two years, with an average of €25.5 million per property vs. 72 assets in 2018-2019 and an average transaction value of €23.65 million.

Furthermore, new players have entered the market during the last two years, namely Resolution Property, Adventum Group, Supernova, Fortres REIT and Oresa Venture. In total, they acquired properties with a cumulative value of around half a billion euros.

Offices have been the most traded asset class in both analyzed periods, and our forecast shows there is further interest in this type of projects. At the same time, the impressive performance of the industrial and logistics segment and also of food retailers has attracted increased more investor interest on these particular sectors.

The retail market is catching its breath after two years of restrictions

The retail market is catching its breath after two years of restrictions

The retail market has been one of the most affected industries during the pandemic, as several “shocks” have been felt especially by shopping centers (in terms of retail schemes) and by non-food retailers – clothing, accessories, footwear, etc (in terms of retailers’ profile). The F&B segment has also been highly impacted, especially after the introduction of the Covid certificates at the end of last year.

The very good performance of retail parks has led developers to invest even more in such schemes, which will remain in focus on the short and medium term as well. Prahova Value Center (21,900 sqm), Sepsi Value Center (16,300 sqm) or Barlad Value Center (16,300 sqm), all developed by Prime Kapitel-MAS Real Estate are among the most important projects delivered last year. However, it should be noted that this year, we will see the completion of the new shopping centers, after two years without such deliveries: the Colosseum Mall extension in Bucharest (16,500 sqm), which already opened on March 24, and Alba Iulia Mall (30,000 sqm), which is expected to be delivered by Prime Kapital – MAS Real Estate at the end of the year.

The main reasons for concern on the retail market are related to the increasing costs for tenants and to the lower purchasing power of customers. Inflation will put pressure on the rental level and also on the disposable incomes of customers.

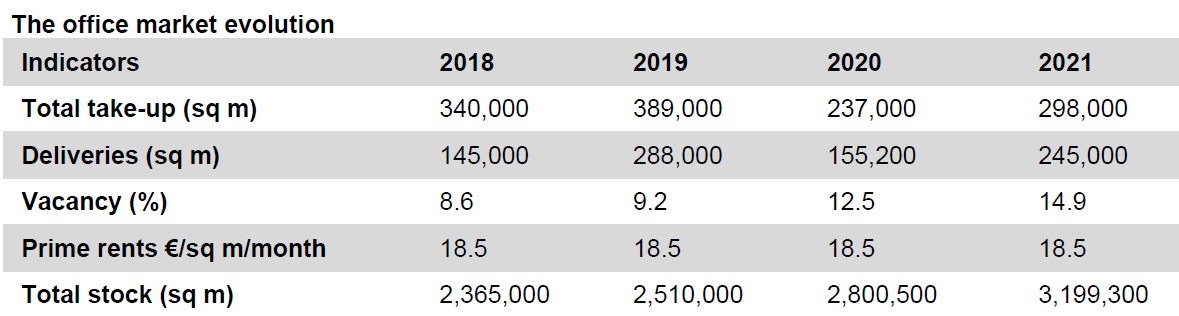

The Office market: Stable rents and new deliveries of 400,000 sqm in the last two years

The Office market: Stable rents and new deliveries of 400,000 sqm in the last two years

Developers continued their pre-pandemic investment plans and completed nearly 400,000 sqm of new office projects between 2020-2021. Therefore, the new supply levels recorded in 2018 and 2019, when a total of 433,000 sqm of new spaces were completed, have generally been maintained the market uncertainty during the pandemic has directly affected the demand, as the total leased area of 535,000 square meters in 2020 and 2021 was 26% below the level recorded in 2018-2019 (729,000 sqm)

Bringing back employees to the office is one of the main challenges at the moment, as landlords, together with tenants, have to find and adopt various measures to persuade employees to return to the office. Reconfiguring existing spaces to provide collaborative areas, as well as creating more spacious offices, are among the most common measures implemented, which translates to an increase in the area allocated per employee from an average of 8-10 to 12-15 sqm/person.

There is also a clear interest towards office spaces that can be instantly occupied (i.e. plug and play), which can be accommodated primarily by Flex Office operators, but also towards spaces available for sublease.

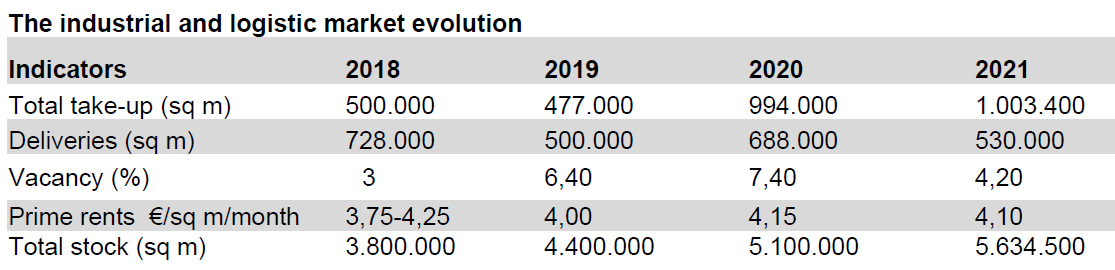

The industrial and logistics market broke all records during pandemic

The industrial and logistics market broke all records during pandemic

Nearly 2 million sqm of industrial and logistics spaces have been transacted over the past two years, double the volume recorded in 2018-2019. This impressive increase of demand encourages developers to continue investing in industrial and logistics projects, with the challenge of adapting the new constructions to the ever-changing tenant requirements.

The tenant profile diversification, especially in the retail sector, (due to the emergence of online retail concerning fresh products), imposes new requirements for storage and distribution facilities. On the other hand, these needs will generate new demand for space.

Other factors putting some pressure on the industrial and logistics market are the increase in construction prices, (of 25-30% on average during the past year) and also the increasing land costs for the development of such projects. Under these circumstances, we are expected to see a rental spike in order for investments in this segment to remain profitable.

However, around 600,000 sqm of new industrial and logistics projects are planned for delivery in 2022.

Cushman & Wakefield Echinox is a top real estate consulting company on the local market and the exclusive affiliate of Cushman & Wakefield in Romania, owned and operated independently, with a team of over 80 professionals and collaborators offering a full range of services to investors, developers, landlords and tenants. For more information, visit www.cwechinox.com

Cushman & Wakefield Echinox is a top real estate consulting company on the local market and the exclusive affiliate of Cushman & Wakefield in Romania, owned and operated independently, with a team of over 80 professionals and collaborators offering a full range of services to investors, developers, landlords and tenants. For more information, visit www.cwechinox.com

Cushman & Wakefield, one of the global leaders in commercial real estate services, with 50,000 employees in over 60 countries and $ 9.4 billion in revenue, provides asset and investment management consulting services, capital markets, leasing, properties administration, tenant representation, project management, design and evaluation services. For more information, visit www.cwechinox.com