European Investment Atlas Q1 2026

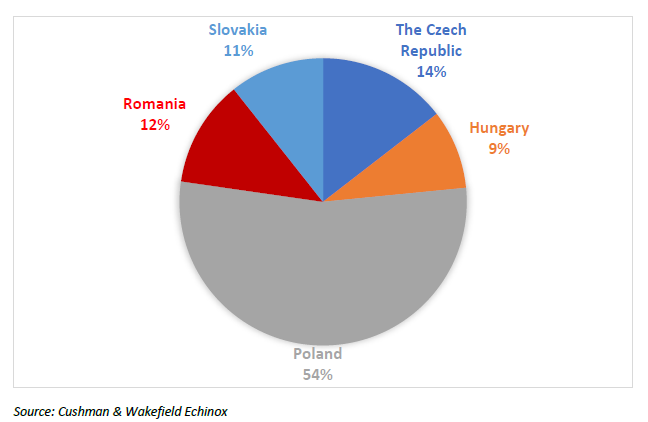

Bucharest, January 2023: The total volume invested in income-producing real estate assets – office, retail, logistics and industrial spaces and hotels – in the Central and Eastern Europe returned to growth last year, a positive evolution mainly driven by the activity recorded in Romania and Slovakia. Romania benefitted from an almost 40% increase of the investment volume, thus moving to the 3rd place in the region (after Poland and the Czech Republic) in this regard in 2022, according to data from the Cushman & Wakefield Echinox real estate consultancy company.

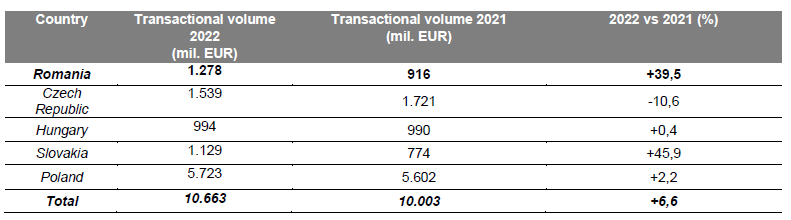

The total transactional volume at regional level reached almost €10.7 billion in 2022, a 6.6% growth compared with 2021, while the market had previously seen a 4.3% contraction in 2021 vs 2020. Almost all countries in the region reported an upward movement in 2022, with the sole exception of the Czech Republic, which experienced a second consecutive year of decline.

Therefore, Poland recorded a growth of 2.2%, while the investment volume in Slovakia was 45.9% higher y-o-y in 2022, with Hungary registering only a marginal increase of 0.4%.

In Romania, even though the number of transactions completed last year was slightly lower compared to 2021 (51 vs. 54), the total investment volume reached a historical record, of almost €1.3 billion, out of which two thirds (€944 million) were signed in H2. A total of 12 properties were the subject of two major office and retail portfolio disposals.

In terms of asset class, the highest number of transactions pertained to office buildings – around 43% of the total (22), followed by retail properties (12). Moreover, 7 industrial and logistics assets have switched owners in the analyzed period.

The average price per transacted property also increased in 2022, reaching €25 million compared with €17 million in 2021. Moreover, the average sale price for office buildings rose by 4.6% to €2,266 /sq m, while the average price for retail properties was of around €1,310 /sq m compared with €973 /sq m in 2021, this in a context where an important number of distressed properties were sold. On the other hand, industrial assets registered a decrease to €405 /sq m versus €503 /sq m in 2021, a fact determined by a lack of transactions with prime properties.

Cristi Moga, Head of Capital Markets Cushman & Wakefield Echinox: “In an environment with many uncertainties, the CEE real estate market continued to be an attractive investment alternative, especially in regards to the main real estate segments – office, retail and industrial. While foreign investors from mature markets, such as the United States, Germany or Sweden, remained dominant in the Polish market, closing the largest transactions, we have noticed an increasing activity of the domestic capital in the other markets. This comes as a result of a better understanding of the market particularities, with the local investors having a higher appetite for risk. As such, almost 40% of the investment volume recorded in the region in 2022 represents acquisitions made by local investors, the most active being Pavăl Holding from Romania (with investments of over €450 million in the country) and Adventum from Hungary (with acquisitions exceeding €350 million in Hungary, the Czech Republic and Poland).”

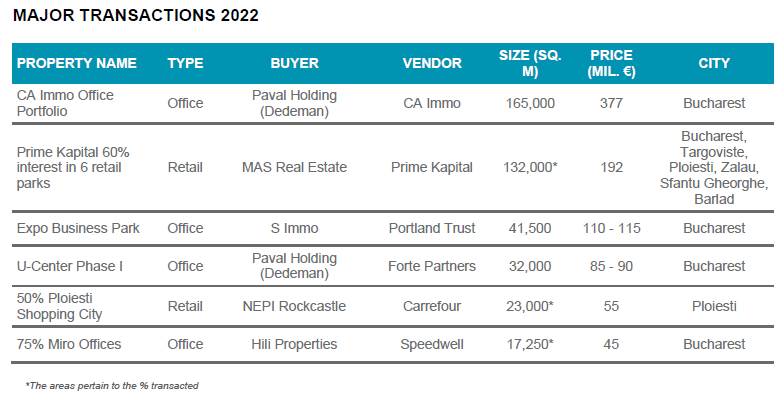

The largest transactions in Romania in terms of volume pertained to CA Immo’s sale of its Romanian office portfolio (6 buildings totaling 165,000 sq. m) to Pavăl Holding Properties (Dedeman Group) and Prime Kapital’s disposal of its 60% interest in 6 retail parks (132,000 sq. m GLA) to MAS Real Estate. The S Immo’s acquisition of the Expo Business Park office project from Portland Trust was the third transaction that crossed the €100 million threshold. These three deals account for more than half of the total volume recorded in 2022 in Romania.

The prime yields have seen an upward movement across all segments due to the increasing financing costs, in line with the trend registered in the entire CEE region, as the office and retail segments recorded a 25 bp spike, with a 15 bp rise for industrial & logistics assets respectively. Even though the increasing interest rates will continue to put pressure on the exit yields, Romania remains an attractive market, as the gap between the local benchmarks and the other CEE markets, such as the Czech Republic, Poland or Hungary is still relatively high in all market segments (generally in the 100 – 250 basis points’ range).

Cushman & Wakefield Echinox is a leading real estate company on the local market and the exclusive affiliate of Cushman & Wakefield in Romania, owned and operated independently, with a team of over 80 professionals and collaborators offering a full range of services to investors, developers, owners and tenants.

Cushman & Wakefield, one of the global leaders in commercial real estate services, with 50,000 employees in over 60 countries and $ 9.4 billion in revenue, provides asset and investment management consulting services, capital markets, leasing, properties administration, tenant representation. For more information, visit www.cushmanwakefield.com