European Investment Atlas Q1 2026

Bucharest, March 2023: The industrial and logistics market registered a new record year both in terms of supply and demand, with development being concentrated in the Bucharest – Ilfov and West regions. However, other areas have also benefited from consistent investments in such projects in the last few years, with demand being mainly driven by logistics and retail companies.

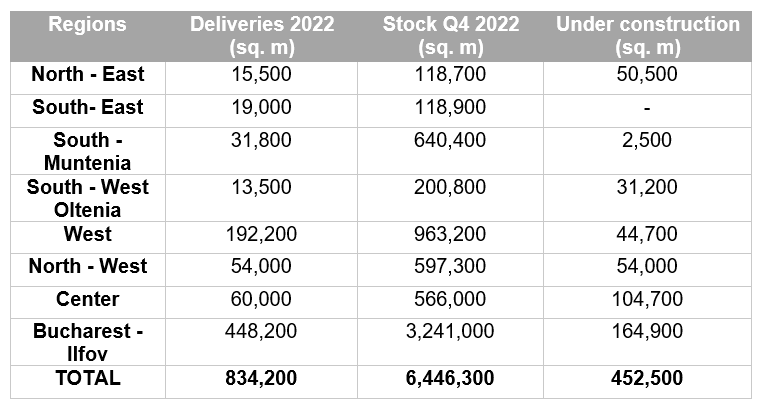

The stock of industrial and logistics spaces in Romania reached 6.45 million sq. m at the end of 2022, with over 90% being located in the Bucharest – Ilfov, West, South – Muntenia, North – West and Center regions, according to the Romania Industrial & Logistics Market report produced by the Cushman & Wakefield Echinox real estate consultancy company.

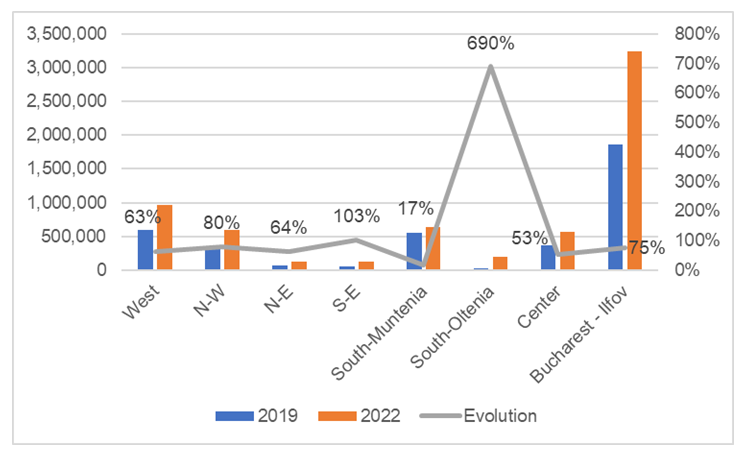

The Bucharest – Ilfov region has a stock of more than 3.24 million sq. m, thus having a market share of more than 50% at national level, being followed by the West (963,200 sq. m), South – Muntenia (640,400 sq. m), North – West (597,300 sq. m) and Center (566,000 sq. m) regions.

The least developed regions in terms of existing industrial and logistics spaces are North – East and South – East (~119,000 sq. m each) and South – West Oltenia (200,800 sq. m), these areas being among the latest ones targeted by developers, an aspect proven by the modern stock growth starting from 2019.

The overall potential of the areas in question is considerably high, given that all developed projects have been almost completely absorbed, with occupancy rates over 95%.

Moreover, the occupancy rate at national level is also around 95%, a robust rate which indicates both a sustained demand (a demand which in the last 3 years amounted to over 3 million sq. m across Romania), while also reflecting the developers’ approach towards less speculative projects, projects which are highly based on pre-lease agreements.

Andrei Brinzea, Partner Land & Industrial Agency, Cushman & Wakefield: ”The last three years have fully illustrated the attractiveness of the local industrial and logistics market, from the perspectives of both tenants and developers. We are very pleased to see more and more destinations benefiting from such investments and currently all geographical regions of the country are actively targeted by market players. It is our opinion that the developers’ expansion plans will continue and they will even intensify as the highway network will expand considerably in areas without such major infrastructure projects, good examples being the A7 Ploiesti – Siret or A8 Targu – Mures – Iasi which will connect the North – East region with the South – Muntenia and Center regions respectively.”

Andrei Brinzea, Partner Land & Industrial Agency, Cushman & Wakefield: ”The last three years have fully illustrated the attractiveness of the local industrial and logistics market, from the perspectives of both tenants and developers. We are very pleased to see more and more destinations benefiting from such investments and currently all geographical regions of the country are actively targeted by market players. It is our opinion that the developers’ expansion plans will continue and they will even intensify as the highway network will expand considerably in areas without such major infrastructure projects, good examples being the A7 Ploiesti – Siret or A8 Targu – Mures – Iasi which will connect the North – East region with the South – Muntenia and Center regions respectively.”

New spaces totalling more than 834,000 sq. m were delivered in 2022, while projects with a total leasable area of at least 452,000 sq. m are expected to be completed across the country by the end of 2023. However, given the dynamics of this segment’s development activity, the 2023 new supply could be even higher than the plans announced by the major market players at the beginning of the year.

Under these circumstances, taking into account the development pace from the last few years and the positive evolution of demand, it is expected that the total stock of industrial and logistics spaces will exceed the 7 million sq. m threshold by the end of this year.

Even though the rising development costs and the increasing energy and land prices continued to put pressure on the new projects’ asking rents, the prime headline level stood between €4.25 – 4.50/ sq. m/ month in Q4 2022, the rental level depending on various criteria such as the occupancy moment, the leased area and also the technical specifications.

We expect to see marginal increases in the following months due to the conservative approaches adopted by developers which are building less speculative projects and also due to a consistent demand for new spaces. The occupier market remains competitive, with a growing interest being also shown for new manufacturing facilities throughout Romania.

Cushman & Wakefield Echinox is a leading real estate company on the local market and the exclusive affiliate of Cushman & Wakefield in Romania, owned and operated independently, with a team of over 80 professionals and collaborators offering a full range of services to investors, developers, owners and tenants.

Cushman & Wakefield, one of the global leaders in commercial real estate services, with 50,000 employees in over 60 countries and $ 9.4 billion in revenue, provides asset and investment management consulting services, capital markets, leasing, properties administration, tenant representation. For more information, visit www.cushmanwakefield.com