European Investment Atlas Q1 2026

Bucharest, May 2026: Romania’s retail market went through a contrasting first quarter in 2026, according to the Romanian Retail Marketbeat Q1 2026 report published by Cushman & Wakefield Echinox. While macroeconomic indicators reflect a period of adjustment, the high street segment and the medium-term development pipeline remain extremely robust.

At the beginning of 2026, inflation reached 9.9%, the highest rate in the European Union, directly impacting retail sales, which declined by 5.8% in real terms. This decrease was driven by a 9.2% drop in non-food product sales and a 2.7% decrease in the consumption of food, beverages, and tobacco. However, analysts anticipate a recovery starting in the second half of the year (H2 2026), as the effects of fiscal measures stabilize, with a year-end inflation forecast of ~5%.

In this context, only one notable completion was recorded during the first three months of the year, namely M Park Titan in Bucharest (8,500 sq. m GLA), developed by M Core, the largest retail project delivered in Bucharest over the past four years.

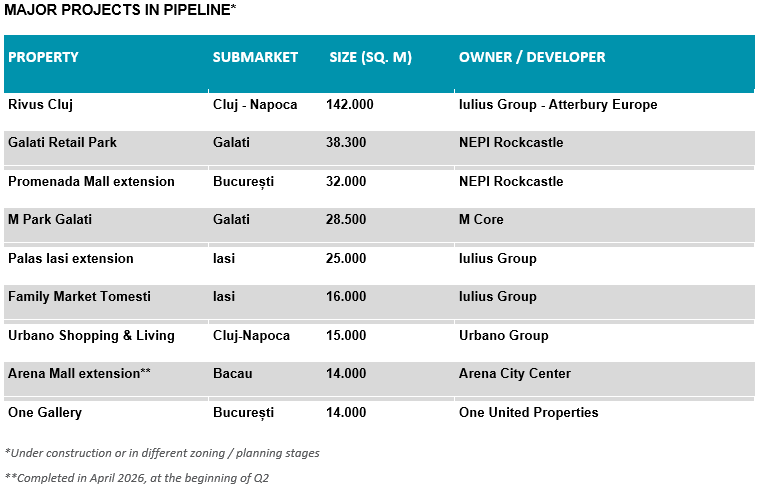

Although the new supply was limited in Q1, developers continue to see a strong potential in the Romanian retail market and are thus investing in new projects, with more than 320,000 sq. m of retail spaces currently under construction nationwide. Approximately half of this total (~150,000 sq. m) is scheduled for delivery by the end of 2026, maintaining the strong development pace seen in recent years.

Among the major projects under construction or in advanced planning stages are Rivus Cluj (142,000 sq. m), Galati Retail Park (38,300 sq. m), the extensions of Promenada Mall in Bucharest (32,000 sq. m) and Palas Iasi (25,000 sq. m) or M Park Galati (28,500 sq. m).

Romania still offers significant expansion potential, having one of the lowest modern retail densities in Central and Eastern Europe, at just 253 sq. m per 1,000 inhabitants.

Dana Radoveneanu, Head of Retail Agency Cushman & Wakefield Echinox: “Developers’ appetite for new retail projects remains unchanged, even though consumption has been under significant inflationary pressures in the first part of the year. With more than 320,000 sq. m currently under development, there is strong confidence in the long-term potential of the Romanian market, both through shopping center projects and retail parks. It is worth noting that the currently under construction projects also include extensions of schemes which have already produced solid returns in cities such as Bucharest, Iasi, or Bacau.”

Dana Radoveneanu, Head of Retail Agency Cushman & Wakefield Echinox: “Developers’ appetite for new retail projects remains unchanged, even though consumption has been under significant inflationary pressures in the first part of the year. With more than 320,000 sq. m currently under development, there is strong confidence in the long-term potential of the Romanian market, both through shopping center projects and retail parks. It is worth noting that the currently under construction projects also include extensions of schemes which have already produced solid returns in cities such as Bucharest, Iasi, or Bacau.”

The prime headline rent for high street spaces on Calea Victoriei continued the robust growth pattern of the last 12 months, now being quoted at €90/ sq. m/ month (+50% y-o-y) as a direct result of new store openings and the expected arrival of major luxury retailers in the coming months. The rental values in dominant shopping centers in Bucharest and in the major regional cities remained stable, generally ranging between €50 – 90/ sq. m/ month for 100 – 200 sq. m spaces located at the ground floor of those respective projects.