Romanian Investment Marketbeat H1 2026

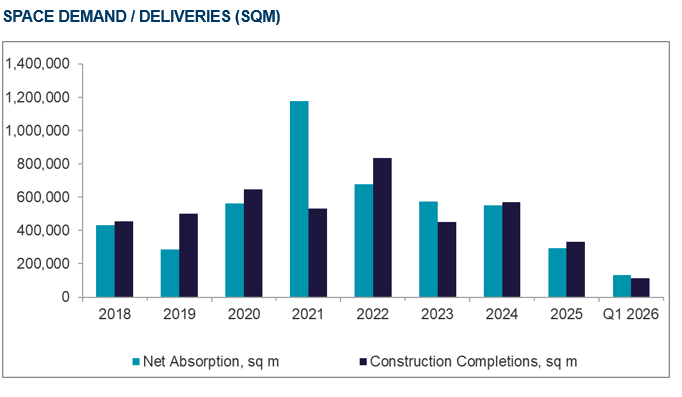

Bucharest, May 2026: The total stock of industrial & logistics spaces surpassed 8 million sq. m across Romania at the end of Q1, confirming the rapid consolidation of this market segment. Approximately 115,000 sq. m of new spaces were delivered in the same quarter, while ~500,000 sq. m are currently under construction, supporting a positive outlook for the remainder of 2026 and the beginning of next year, according to the Romania Marketbeat Industrial Q1 2026 report published by the Cushman & Wakefield Echinox real estate consulting company.

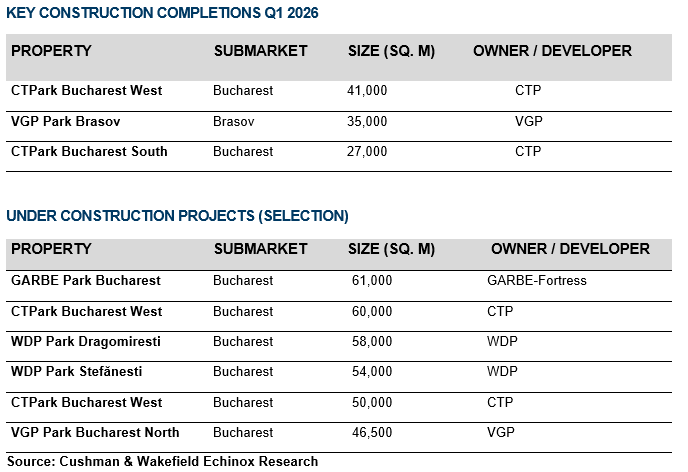

The projects delivered in the first three months of the year are located almost exclusively in Bucharest (~70,000 sq. m) and Brasov (35,000 sq. m).

By the end of the year, the total stock of industrial & logistics spaces across Romania is expected to exceed 8.5 million sq. m.

More than 400,000 sq. m of new projects are currently under development around Bucharest, meaning that the capital city’s stock will surpass the 4 million sq. m threshold by the end of 2026. One of the largest projects which kick-started construction in Q1 is the first industrial & logistics park developed by the German group GARBE (in partnership with Fortress) in Romania (in northern Bucharest), a project exceeding 60,000 sq. m GLA.

At the same time, the leasing activity totaled 240,000 sq. m in Q1 2026, reflecting a moderate 7% decrease compared with the same period of 2025. However, if this volume is maintained throughout the remaining quarters, the 2026 take-up could reach ~1 million sq. m, in line with the last 6 years’ average.

The structure of transactions in Q1 2026 highlights a positive trend, with approximately 58% of the total volume generated by new demand (140,000 sq. m), illustrating the tenants’ continued interest and confidence in developing and optimizing their logistics operations.

Bucharest had the highest share in demand, accounting for nearly 55% of the total transacted volume nationwide. Timisoara ranked second, with a 22% share of the total.

The overall vacancy rate stands at approximately 5.4%, a healthy level for the market.

Prime rents remained stable in Bucharest and in key regional industrial & logistics hubs — Cluj-Napoca, Timisoara, Brasov and Ploiesti — ranging between €4.50 and €4.75/ sq. m/ month.

These levels could see upward adjustments in the coming quarters amid inflationary pressures and rising land prices, factors that continue to influence development decisions.

Rodica Târcavu, Partner Industrial Agency, Cushman & Wakefield Echinox: “On the short term, Romania’s industrial & logistics market is experiencing the effects of an uncertain economic environment and a more cautious approach from tenants, which explains the slight slowdown in leasing activity. However, the fundamentals remain strong, as we continue to notice active demand from both international and local companies. Firms contracting industrial & logistics spaces operate across diverse sectors, including general goods distribution, courier services, logistics and light manufacturing. On the medium term, we expect the market to remain on a growth trajectory, supported by the clarification/ resolution of international conflicts and greater economic and political predictability both globally and nationally.”

Rodica Târcavu, Partner Industrial Agency, Cushman & Wakefield Echinox: “On the short term, Romania’s industrial & logistics market is experiencing the effects of an uncertain economic environment and a more cautious approach from tenants, which explains the slight slowdown in leasing activity. However, the fundamentals remain strong, as we continue to notice active demand from both international and local companies. Firms contracting industrial & logistics spaces operate across diverse sectors, including general goods distribution, courier services, logistics and light manufacturing. On the medium term, we expect the market to remain on a growth trajectory, supported by the clarification/ resolution of international conflicts and greater economic and political predictability both globally and nationally.”